The House Judiciary Committee on Tuesday abruptly postponed a markup.

Source: GOP panel delays tort reform bill after conservative backlash | TheHill

The House Judiciary Committee on Tuesday abruptly postponed a markup.

Source: GOP panel delays tort reform bill after conservative backlash | TheHill

[N]either laws nor the procedures used to create or implement them should be secret; and . . . the laws must not be arbitrary. —U.S. Court of Appeals Judge Diane Wood, “The Rule of Law in Times of Stress” (2003)

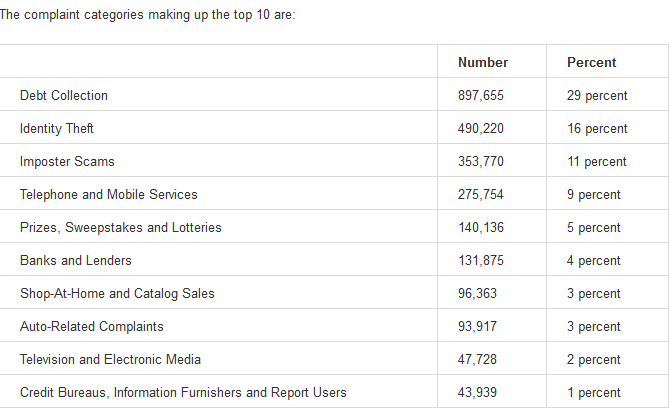

On a somewhat regular basis the Federal Trade Commission also known as the FTC provides a list of information that they have been compiling. Specifically, they provided a list of the top ten consumer complaints according to complaints that they have received from consumers.

As can be seen, debt collection identity thefts are the top two complaints. These are complaints that consumers have complained about to the Federal Trade Commission. The Federal Trade Commission then will take these complaints and make investigations. Sometimes the Federal Trade Commission will then file lawsuits and issue orders and sometimes they do not. The Federal Trade Commission has a website contained therein the numerous investigations complaints which they are taken and pursued under the authority of the federal government. Obviously, debt collectors are one of their top targets. The issues with debt collectors are frequently harassing and deceptive collecting techniques.

Does a business such as a law firm, gas station, boutique or other ongoing business entity have the right to sue under the New Jersey Consumer Fraud (CFA) (UDAP) Act when they have been a victim of consumer fraud? YES

The answer is yes under most circumstances. The courts have interpreted the New Jersey Consumer Fraud Act to apply to businesses (as a plaintiff) as they acting a a regular consumer. If a business is like in consumer and consuming a good then they are able to pursue a claim under the New Jersey Consumer Fraud Act. This business would have the same rights as any other person which would be triple damages, attorney’s fees and costs. This would be assuming that the business demonstrate an ascertainable loss related to the fraudulent conduct. Just because plaintiff is a business does not rule them out from being a plaintiff in a case.

The sole issue is whether or not the business is acting as a consumer or business. As an example, there was a case which was decided in the New Jersey courts that held as a re seller of ink cartridges there were no claims under the New Jersey Consumer Fraud Act. In that transaction the court held that business which had filed suit under the New Jersey Consumer Fraud Act was acting as a business and reselling the ink cartridges rather than consuming them.

Does New Jersey have a Lemon Law? Yes there is a new and used car lemon law that can be filed in Superior Court or in Administrative Court … – The Law Office of Jonathan Rudnick LLC – Google+

Source: Does New Jersey have a Lemon Law? Yes there is a new and used car lemon law …

Bergen County Verdict in a car sales case

$174,000 verdict for purchaser who did not get the title

www.consumer-attorney.com

CONSUMER PROTECTION

11-4-9287 Mehrnia v. Emporio Motor Group LLC, Chanc. Div.-Bergen Cnty. (Toskos, J.S.C.) (24 pp.) This case evolved from a dispute between several parties over their rights to the ownership of a used 2010 Ferrari. The car was sold several times. Plaintiff Mehrdad Mehrnia claimed that he purchased the vehicle for a price of $201,000. Defendant Hitfigure LLC claimed ownership of the 2010 Ferrari through a subsequent purchase for a price of $155,000. The dispute arose from the relationship between defendants Dream Cars National LLC and Gotham Dream Cars LLC and defendant Manhattan Leasing Enterprises Ltd. Gotham and Manhattan also claimed an ownership interest in the vehicle. At a time when Gotham was experiencing financial difficulties, Manhattan restructured their leasing arrangement, which led to Manhattan obtaining possession of the title to the 2010 Ferrari. Mehrnia purchased the car from Emporio Motor Group LLC, which had obtained the Ferrari from Manhattan. The Ferrari was later sold to Hitfigure. Mehrnia filed this litigation seeking a declaratory judgment that he was the owner of the Ferrari. He also asserted a consumer fraud and conversion claim against Gotham and Manhattan. Finally, Mehrnia included a civil conspiracy claim as to Emporio, Gotham and Manhattan, alleging that they conspired to deprive Mehrnia of his property.

FACTS – SUMMATION

The plaintiff has proved that the defendant has committed fraud/consumer fraud. The dealer advised the plaintiff that the car was without accident both verbally and in writing. The plaintiff proved (CARFAX) and it was admitted (Defense expert testimony) that the car was in a previous accident. Defense only disputed severity of the accident. Defense expert and the General Manager admitted that the dealer probably knew of the prior damage. He actually testified that the dealer did know that the car was in an accident. The car was inspected by used car manager, technicians, certification process (Lexus trained techs looking for accident damage) and elcometer use on car acquisitions. (THE USED CAR MANAGER NEVER TURNED UP TO TESTIFY) Even more significant is that this was a dealer not a Chevy dealer!! Who would be in a better position to know that the car was not in MFGR-HIGHLINE- FRONT LINE CONDITION? Nobody. The dealer’s claim or assertion of ignorance as to any prior damage is both insulting and incredulous. The Manufacturer representative testified that bondo should not be used on certified cars (not Lexus quality repair) and any through panel penetration would render a car non-certifiable. (This was his initial testimony and then there was a break and Ms. Lawyer asked him the same question and his answer mysteriously changed)

NEW JERSEY LAW AND THE CONSUMER FRAUD ACT

NO DIRECT CONTACT IS REQUIRED BETWEEN THE DEFENDANT AND THE CONSUMER

THE DEFENDANT’S ASSERTION THAT THEY ARE NOT SUBJECT TO THE CONSUMER FRAUD ACT BECAUSE THEY DID NOT DIRECTLY SELL OR HAVE ANY DIRECT CONTACT WITH THE PLAINTIFF IS NOT SUPPORTED BY THE LAW, INCLUDING THE DEFINITION SECTION OF THE CONSUMER FRAUD ACT

A. NO DIRECT RELATIONSHIP OR CONTRACT IS REQUIRED BETWEEN THE PLAINTIFF AND DEFENDANT TO MAINTAIN A CLAIM UNDER THE CFA

The lack of a contractual relationship or privity does not automatically defeat a the plaintiff’s claim. The determination of whether a duty exists is generally considered a matter of law to be decided by the court. Carvalho v. Toll Bros. and Developers, supra, 143 N.J. at 572; S.P. v. Collier High School, 319 N.J.Super. 452, 467,(App.Div.1999). The assessment of fairness and policy “involves identifying, weighing, and balancing several factors-the relationship of the parties, the nature of the attendant risk, the opportunity and ability to exercise care, and the public interest in the proposed solution” Zielinsky v. Professional Appraisals 326 N.J.Super 219 (App.Div 1999).

There is no privity requirement to maintain a cause of action under the New Jersey Consumer Fraud Act. In Alloway v. General Marine Ind., 149 N.J. 620 (1997), the Supreme Court held that the New Jersey Consumer Fraud Act does not require privity to maintain a cause of action. In Alloway, the plaintiff purchased a defective boat, which was built by the (manufacturer) defendant. The plaintiff instituted suit against the manufacturer and other defendants for tort (negligence) and warranty claims. The Court dismissed the tort claims and permitted the plaintiff to proceed on the warranty claims, holding that privity was required for tort claims, but not for warranty type claims. The underpinnings of the decision were that the plaintiff had statutory avenues of remedy including, but not limited to, the Uniform Commercial Code (UCC) and the New Jersey Consumer Fraud Act to address economic injuries to property. Id. at 639 – 640. The Court specifically left unanswered whether or not tort or contract law applies to a product that poses a risk of causing personal injuries or property damage, but has caused only economic loss to the product itself.

The trend in the application of the Consumer Fraud Act has been to expand liability to those “upstream, in the chain of commerce,” including but not limited to remote suppliers of component parts whose products are passed on to a buyer and its representations are made to, or intended to be conveyed to the ultimate purchaser. Perth Amboy Iron Works v. Amhouse, 226 N.J. Super 200, 211 (App. Div. 1998).

THE REMEDIES PROVIDED IN THE NEW JERSEY CONSUMER FRAUD ACT ARE CUMULATIVE AND, IN ADDITION TO ANY REMEDIES CONTAINED IN THE UNIFORM COMMERCIAL CODE, THUS THE CLAIMS ARE NOT MUTUALLY EXCLUSIVE

The rights provided under the New Jersey Consumer Fraud Act are in addition to any other statutory or common law rights. N.J.S.A. 56:8-2.3 which provides as follows:

The rights, remedies and prohibition accorded by the provisions of this Act are hereby declared to be in addition to and cumulative above any other rights, remedies or prohibition accorded by the common law or statutes of this State, and nothing contained herein shall be construed to deny, abrogate, or impair any such common law or statutory right, redress or prohibition.

The clear intent of the New Jersey Consumer Fraud Act was to provide consumers with additional and cumulative remedies and in no way curtail their remedial opportunities for the redress of fraud and other unconscionable practices afforded by any other statute or common law. Cybul v. Atrium Palace Syndicate, 272 N.J. Super. 330, 335 (App. Div. 1994).

In Cybul, the Appellate Division held that the plaintiff could maintain a cause of action under an administrative scheme wherein there was no direct provision for a cause of action to the plaintiff. In Lemelledo v. Beneficial Management, 150 N.J. 255 (1997), a watershed case, the New Jersey Supreme Court held that the plaintiff could maintain a private cause of action in addition to a statutory scheme which provided the plaintiff only a return of premiums paid under the policy. The New Jersey Supreme Court held that: “The CFA simply complements those statutes, allowing for regulation by the Division of Consumer Affairs and a private cause of action to recover damages. The damages cause of action in no way inhibits enforcement of other statutes, because a Court can assess damages in addition to any other penalty to which a defendant is subject.” Continue reading ›